By: Jase Casias | June 29th, 2026

Six months into 2026. Here is what has actually happened across the sectors we serve, and what it signals for hiring through the rest of the year.

Civil, Structural and Construction Management

The Bipartisan Infrastructure Law is now in peak delivery phase. Projects that spent three to five years in design and permitting are finally breaking ground, and that is pulling on a labor market that was already operating near capacity.

- 92% of AEC firms reported difficulty filling both craft and salaried positions in the latest AGC workforce survey.

- There are currently 3 engineering jobs for every 1 qualified candidate in the market.

- Senior engineering roles are averaging 40 to 50 days to fill, and that number is not improving.

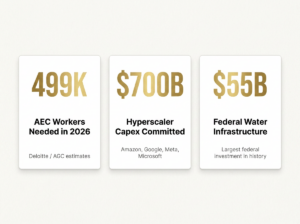

- An estimated 41% of the current construction workforce is eligible to retire by 2031. The knowledge transfer problem is now a project delivery risk.

“The talent competition has gotten more vertical. Data center projects now compete directly with water infrastructure, semiconductor manufacturing, and grid modernization for the same pool of experienced project managers.”

Water and Wastewater

The IIJA directed $55 billion to water infrastructure, the largest federal investment of its kind in U.S. history. The capital is flowing. The people who can execute the work are the constraint.

- Civil engineers, water and wastewater process engineers, and design managers are in short supply at both utility owner and consulting firm levels.

- 30 to 50% of the water workforce is eligible to retire within the decade.

- The IIJA water authorization expires in September 2026. Reauthorization is not certain. Projects already under contract are protected. Firms that have not yet mobilized on programmed work face real uncertainty.

Data Center Construction

The four major hyperscalers committed $700 billion in combined capex for 2026, a 77% increase from 2025. That money flows directly into construction. U.S. data center construction spending hit a monthly run rate of $45.1 billion by December 2025, up 85% from two years prior.

- 340,000 data center positions are projected unfilled by end of 2026.

- MEP engineer vacancies are averaging 4.2 months to fill.

- Commissioning engineers and MEP-experienced estimators are the two hardest seats to fill in the entire industry right now.

Oil and Gas, Manufacturing, Telecom

These sectors are on our horizon because the talent profiles overlap directly with our core AEC and Digital Infrastructure community. Civil and structural engineers, construction managers, and project leaders move between these disciplines regularly, and IRG is building the practice depth to serve them. Future issues will go deeper in each.

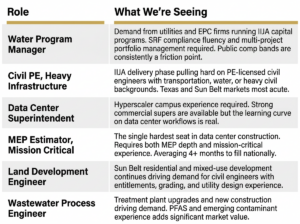

ROLES TO WATCH

The Hardest Seats to Fill Right Now

COMPENSATION WATCH

Where Pay Has Moved in 12 Months

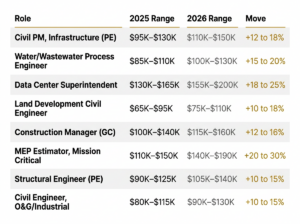

Directional base salary ranges for mid-career to senior experienced candidates (approximately 7 to 15 years of experience) in private-sector AEC and infrastructure roles across U.S. markets. Ranges are consistent with the ASCE 2025 Civil Engineering Salary Report, Deloitte 2026 Engineering and Construction Outlook, and U.S. Bureau of Labor Statistics occupational data. Total compensation including bonus and benefits typically adds 15 to 25%. Public-sector and utility roles will fall below these ranges in most markets.

ON THE HORIZON

Five Things to Watch in H2 2026

- IIJA Water Reauthorization

The authorization expires September 2026. Reauthorization is uncertain. Firms and utilities that have not mobilized on programmed work face real schedule risk. Watch state-level SRF activity as a leading indicator of where project flow continues regardless of federal action.

- Renewable Energy Construction Surge

The phaseout of 45Y and 48E tax credits for projects beginning construction after July 4, 2026 is triggering a front-loaded construction rush right now. This creates a short-term spike in renewable construction labor demand followed by a potential lull as the uncreditable pipeline rationalizes. Staff thoughtfully.

- Hyperscaler Capex Absorption

$700 billion in committed capex is an extraordinary number. The real constraint is execution capacity. Expect GCs and specialty contractors to consolidate mission-critical talent aggressively in H2, and per diem and relocation packages to continue escalating in Phoenix, Columbus, and the broader Sun Belt.

- Texas Infrastructure Concentration

The Texas Triangle is among the most active infrastructure hiring markets in the country. Data center expansion, grid modernization, IIJA civil work, and continued land development are all pulling from the same regional talent pool. Comp pressure in Texas has been consistently above national averages for 18+ months.

- Oil and Gas Construction Pickup

Midstream and facility construction in the Permian Basin is active. Civil and structural engineers with pipeline, pump station, and facility backgrounds are in demand. Firms that have historically operated in either AEC or O&G but not both are now competing for the same candidates.

Connecting Those Who Connect Us

irgtalent.com | Infrastructure Intelligence publishes the last Monday of every month

Compensation ranges reflect mid-career to senior experienced candidates (approximately 7 to 15 years of experience) in private-sector AEC and infrastructure roles. Consistent with ASCE 2025 Civil Engineering Salary Report, Deloitte 2026 Engineering and Construction Outlook, and U.S. Bureau of Labor Statistics data. Provided for informational purposes only. Copyright 2026 Infrastructure Recruitment Group.